Today, the optimism has faded, washed away by a deluge of debt.

Essential to the plan were the “Big Three” U.S.-based credit rating agencies — S&P Global Ratings, Moody’s Ratings and Fitch Ratings, which together account for more than 90% of global ratings. The rating agencies collected fees for their services and began applying their complex analyses to the region.

Given the troubled economic history and conditions of sub-Saharan Africa, it came as little surprise that the Big Three gave most countries below-investment-grade, or “junk,” ratings. Those low scores meant the countries had to pay higher interest rates on their bonds to attract investors who might otherwise balk at the risk. The thinking at the time was that African countries’ ratings would improve, and their cost of borrowing decline, as their growing economies allowed them both to repay their debts and invest in development.

Instead, the push for credit ratings set these nations on a path to debt many could not afford. Over the past two decades, more than a dozen sub-Saharan countries borrowed nearly $200 billion from overseas bond investors, according to World Bank figures. As their nations’ finances faltered, African leaders lashed out at the rating agencies with allegations that the firms were biased in their assessments. Reuters did not find evidence of systemic bias in the Big Three’s ratings for the region. Rather, Africa’s debt crisis highlights the potential pitfalls when sophisticated financial markets meet impoverished countries eager for development.

After dozens of interviews with current and former Big Three employees, large investors and officials with government and multinational organizations, along with a review of hundreds of pages of regulatory and legal filings, Reuters found that the Big Three weren’t fully prepared for the challenges of rating a region awash in poverty and unfamiliar with the process, and that many of the nations involved weren’t ready for the torrent of cash their credit ratings unlocked.

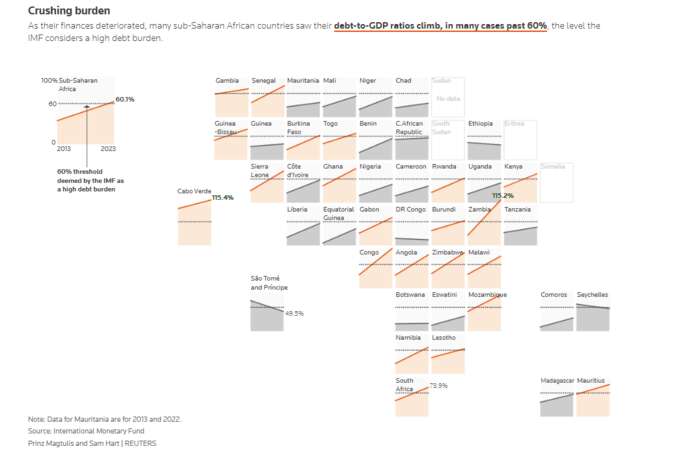

The upshot: Billions of dollars meant to pay for badly needed improvements to infrastructure, education and healthcare are now going toward interest payments. Sub-Saharan Africa’s average debt ratio has almost doubled in the past decade — from 30% of gross domestic product at the end of 2013 to nearly 60% in 2022. The region today has the highest rate of extreme poverty in the world.

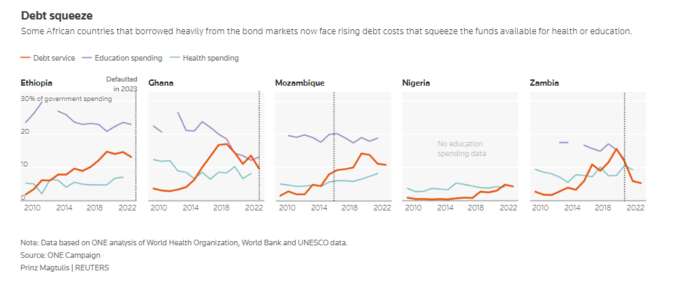

When debt service crowds out spending on infrastructure and other public goods, “the country doesn’t grow, and you just end up in a vicious cycle of poverty,” said Christopher Egerton-Warburton, founding partner of Lion’s Head Global Partners, a London-based investment bank that has advised African governments.

The financial burden carries deadly potential. In June, anti-government riots exploded across Kenya in protest against proposed tax increases, including levies on bread, cooking oil and other staples, to help fund payments on the roughly $80 billion Kenya owes creditors. The rioting, which continued after the proposal was withdrawn, left dozens dead and many more injured.

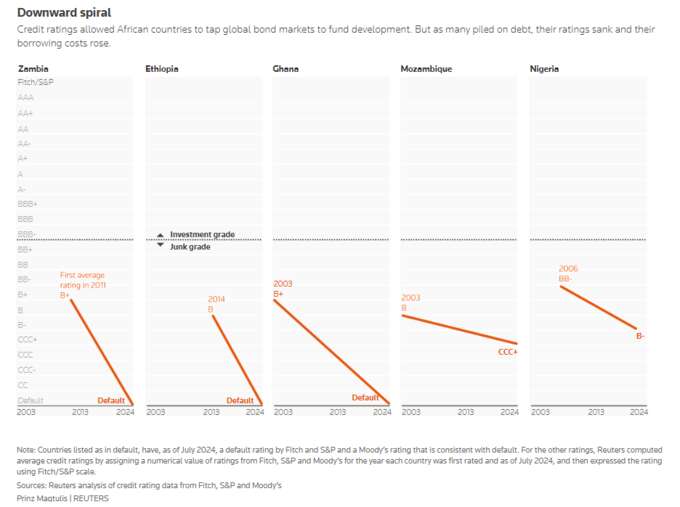

Bad luck plays a part in Africa’s debt debacle. Some nations weren’t ready when prices plunged for commodities that underpin their economies. After the COVID-19 pandemic shuttered the global economy, cautious bond investors pulled back. The Big Three slashed ratings for many sub-Saharan countries. Then as global inflation pushed upward, major central banks raised interest rates, increasing borrowing costs. Several African nations ended up defaulting on their bonds or struggling to pay debts.

That’s what happened to Ghana, a top cocoa producer. It defaulted on most of its external debt in 2022, after rising debt costs prompted Moody’s to cut its credit rating. At the time, Ghana said its interest payments were consuming up to 100% of government revenue.

After the downgrade, Ghana’s Finance Ministry took aim at Moody’s, issuing a statement in which it alleged “institutionalized bias,” and declared, “We shall actively continue to support the global outcry against this leviathan.”

The ministry publicly named the Paris-based lead analyst for Ghana and her supervisor, and asserted that she had not visited Ghana since Moody’s assigned her to it earlier that year.

Moody’s declined to comment on the episode. Neither the analyst nor her supervisor responded to requests for comment.

In its reaction to the downgrade, Ghana joined a growing chorus of criticism of the Big Three from African leaders as they watched their already low credit ratings wilt and funding streams dry up. Then-Senegalese President Macky Sall in 2022 decried “the sometimes very arbitrary ratings.” Kenyan President William Ruto said last year that the process “needs to be overhauled.” In a statement to Reuters in March, Finance Minister Wale Edun of Nigeria said: “The concern is that the methodologies employed may not be consistently applied across the board, particularly for African countries.”

Reuters asked officials from the four countries for evidence to support allegations of bias. None provided any.

S&P declined to comment for this article. After repeated requests for comment, Moody’s sent Reuters a brief statement in which it said: “We stand by the performance of our sovereign credit ratings, the application of our global methodology, and the rigorous processes we employ to ensure their accuracy, independence, and integrity.”

In an interview with Reuters, Jan Friederich, Fitch’s Hong Kong-based head of sovereign ratings for Europe, the Middle East and Africa, said African leaders’ assertions of bias are based on the misapprehension that all regions share similar risk profiles and should have similar credit ratings. “Our response, of course, is that it’s not the ratings that are unusually distributed,” he said. “It’s the African countries that have unusual features.”

Friederich noted, for example, that for 2023, government debt in sub-Saharan Africa was about 340% of revenue — by far the worst of any region in the world. “For economies that have such features that are so distinct … it should be no surprise that there is a significant difference in creditworthiness,” he said.

‘NO CLEAR, OUTRIGHT BIAS’

Reuters reviewed research on global sovereign ratings and found no evidence of bias in the Big Three’s ratings for sub-Saharan Africa. Ten academics, analysts and economists who built models to replicate the firms’ rating process told Reuters in separate interviews and notes that they found no meaningful inconsistencies between Big Three ratings assigned to sub-Saharan countries and ratings suggested by their own models.

While the rating agencies do not publish their models in their entirety, they have described them in enough detail for researchers to reliably reproduce them — a blend of quantitative analysis of factors like a nation’s debt burden, and qualitative assessments of governance and institutional strength. Neither the 10 researchers, nor 20 additional economists and academics interviewed about the modeling, including critics of the rating agencies, were able to refer Reuters to any studies that found bias by applying a ratings methodology similar to those published by the rating agencies.

I never doubted that there were going to be defaults.

David Beers, S&P’s former global head of sovereign ratings

“There is no clear, outright bias towards African countries in terms of credit ratings,” said Oliver Takawira, a University of Johannesburg economist who co-wrote a paper examining two decades of ratings for South Africa. Takawira said his model matched the rating agency’s conclusions 93% of the time.

Still, he said, he understood the frustration of African countries. They “do not know what methodologies or criteria are used by credit rating agencies,” Takawira told Reuters. That leaves them feeling vulnerable, and they assume the low ratings result from bias, he said.

In the credit rating process, the Big Three must collect masses of reliable, standardized data, information that is hard to come by in many African nations with large, untracked informal economies. Nearly all agency analysts work in capital cities or financial centers outside of Africa — places like New York, London and Hong Kong. And ratings can be undercut by the lack of government transparency, endemic corruption, political instability and civil strife that afflict parts of the region.

Fitch has no offices in Africa. On their websites, Moody’s and S&P list only offices in South Africa; combined, the two companies have a handful of affiliates operating on the continent. In the European Union, regulations require that agencies assessing countries and key institutions have a physical presence in the bloc.

Friederich, the Fitch executive, said it’s not feasible to have an office in every African country, and that given the continent’s infrastructure challenges, it’s not “always easier to fly from one place in Africa to another, than from outside of Africa.”

At the U.N. Development Programme, the agency instrumental in the push to get credit ratings for sub-Saharan nations, senior economist Raymond Gilpin disagreed, saying it was “unconscionable” that the Big Three didn’t have a larger presence on the continent. At the same time, he said he saw no bias in the way the Big Three apply their methodologies, and he echoed other officials and academics when he told Reuters the rating agencies’ work can be hampered by local realities.

He and others familiar with the ratings effort said that many African countries lack the basic requirements for the process, such as sophisticated, reliable datasets. Rating agencies are “not going to get the clear sense of what risk actually is in those contexts,” said Gilpin, head of the UNDP’s strategy, analysis and research team for Africa. “That’s not the fault of the agencies. It’s just the landscape in which they operate.”

Early in the initiative, Gilpin said, doubts about the African nations’ ability to meet the demands of the rating process were outweighed by the belief that “having their sovereign ratings done is a positive thing” for meeting development goals.

When asked about the U.S. role in securing sovereign credit ratings for Africa and what ensued, Joy Basu, a U.S. deputy assistant secretary of state for African affairs, said in a statement to Reuters: “The international rating agencies play a critical role in unlocking private credit.” She added: “It is important that the ratings’ inputs are objective and transparent — and applied fairly amongst regions." She did not specifically address claims of Big Three bias.

Some Big Three executives told Reuters that from the start, they saw trouble coming. These were countries with an uneven borrowing history, said David Beers, S&P’s global head of sovereign ratings when the initiative began with the U.N. Development Programme. “I never doubted that there were going to be defaults,” said Beers, now retired.

He and Fitch’s Friederich pointed out that their firms provide a ratings service for a fee, and it’s up to nations and investors to take it from there.

‘A TICKET TO THE BENEFITS’

About 30 years ago, the Heavily Indebted Poor Countries Initiative, spearheaded by the World Bank and the IMF, began the process of wiping more than $100 billion of debt off the books for nearly 40 countries, most of them in sub-Saharan Africa, through a combination of loans, grants and buybacks. In return, the debtor nations had to commit to policy changes and poverty reduction.

To fund development moving forward, the Eurobond market, where money can be raised quickly, was widely seen as the natural choice, said Zephirin Diabre, a Burkina Faso economist who worked on the ratings push while at the UNDP. Eurobonds — debt securities denominated in a currency other than that of the issuer’s home country, usually U.S. dollars — accounted for at least $113.5 billion of bonds issued by sub-Saharan countries since 2004, according to JPMorgan figures.

“The World Bank can’t give them all that money in concessional loans” — that is, loans at lower-than-market interest rates, Diabre said.

The U.S. government championed the idea of credit ratings for sub-Saharan Africa. At a 2002 State Department conference in Washington, D.C., then-Secretary of State Colin Powell told an audience that included many African officials: “A sovereign credit rating can be your country’s ticket to the benefits of the global economy and to the capital flows that exist in the global economy, and we are here today to help you earn that ticket.”

The U.S. government partnered with Fitch, picking up the initial tab for country evaluations. The UNDP did the same with S&P.

For an African nation, ratings “would signal to various types of investors around the world that the government was prepared to be more forthcoming” about its economy and public finances, said Beers, the former S&P executive. Many investors are prevented by regulations from buying bonds of issuers that don’t have Big Three ratings.

For the Big Three, the program bore little downside. From 2003, S&P initiated ratings for more than 20 sub-Saharan nations — business that Beers said enriched the firm’s bottom line.

Early attention focused on two of the region’s largest economies: Ghana, a source of oil, gold and cocoa, and Nigeria, Africa’s top oil exporter and most populous nation.

Ghana was one of the first to get a rating under the program. In 2003, S&P gave it a B+ with a stable outlook. That’s four rungs below investment grade, but given the nation’s bright prospects at the time, its leaders were enthusiastic. “To ask if Africa is ready for portfolio investment is to ask a starving man if he is ready for food,” Ghana’s finance minister said at a 2003 event in New York organized by the UNDP with the New York Stock Exchange.

Four years later, Ghana made its market debut, raising $750 million through a sale of Eurobonds. Investors were drawn to the 8.5% coupon, almost twice the rate on the benchmark 10-year U.S. Treasury notes; demand for the Ghanaian bonds was four times greater than the amount offered.

In 2006, S&P gave Nigeria a rating of BB-, one notch above Ghana’s. In 2011, the country issued its first Eurobond, for $500 million. It was more than 2.5 times oversubscribed. Nigeria then raised $1 billion more in two separate bond issues that were also oversubscribed.

“Bondholders really welcomed them with open arms,” said Giulia Pellegrini, senior portfolio manager for emerging market debt at Allianz Global Investors.

The enthusiasm seemed justified. Ghana’s economic growth hit 14% in 2011, the fastest in the region. Nigeria’s growth was at a strong 5.3% and showing signs of improvement.

By this time, Moody’s — the last among the Big Three to expand its portfolio of sovereign ratings in sub-Saharan Africa — had begun to seek a bigger footprint in the region.

In August 2010, Moody’s hired Nigerian economist Weyinmi Omamuli to join its sovereign risk team as a London-based vice president and senior analyst. Omamuli had degrees from the London School of Economics and experience at a Nigerian investment firm and at Britain’s finance and international development ministries. She was initially assigned to cover Nigeria, Kenya and other countries.

Omamuli soon came to believe that Moody’s slow start in sub-Saharan Africa resulted in part from ambivalence toward the continent, according to her witness statement in a race and disability discrimination claim she brought against Moody’s and one of its executives in a London tribunal. The case was settled in 2015; terms were not disclosed.

In her witness statement, a copy of which was seen by Reuters, Omamuli — now a senior economics adviser at the UNDP — wrote that senior Moody’s staff expressed negative views of countries in the region. In 2010, she wrote, Michael Korwin, then a Moody’s business development executive, told her that when the firm was first approached about rating sub-Saharan nations around 2002, "the proposal was ‘laughed out of the door,’ or words to that effect” and that it seemed “utterly ridiculous” at the time to think sub-Saharan countries could access global capital markets.

Omamuli wrote that Korwin told her Moody’s began its push into sub-Saharan Africa only because the firm “was now keen to find new revenue sources.”

Around the same time, a senior Moody’s analyst recounted that her husband traveled to Lagos, Omamuli’s hometown, and said it was “a dump,” she wrote.

Contacted by phone, Korwin, now retired, called Omamuli’s recounting of his remarks “pure myth.”

“I, as a marketing person, would not have been privy to senior management discussions where anyone in New York or London would make the decision,” said Korwin, who left Moody’s in 2017. He was not the executive against whom Omamuli filed her discrimination claim.

Korwin said that Moody’s, while slower than its competitors to expand in sub-Saharan Africa, ramped up its efforts in response to investor demand. “At the end of the day, you serve a purpose to the investor community, which drives your business plan,” he said.

A former Moody’s executive who requested anonymity echoed the skepticism Omamuli described. Countries in the region “didn’t have a clue what we were doing,” this person said. “It was definitely too early” for the region’s governments to quickly take on and manage masses of private debt, which they might struggle to repay when interest rates went back up. But for many countries, the former executive said, being wooed by big-name investors was “just intoxicating.”

ALLURING TO INVESTORS

All told, 22 African countries were assigned Big Three ratings in the decade ending in 2010. With interest rates at historic lows after the global financial crisis, African countries could count on strong investor demand for their comparatively high-yield debt. Ghana and Nigeria returned to the Eurobond market in 2013. Kenya and Ethiopia debuted in 2014, followed by Angola and Cameroon the next year.

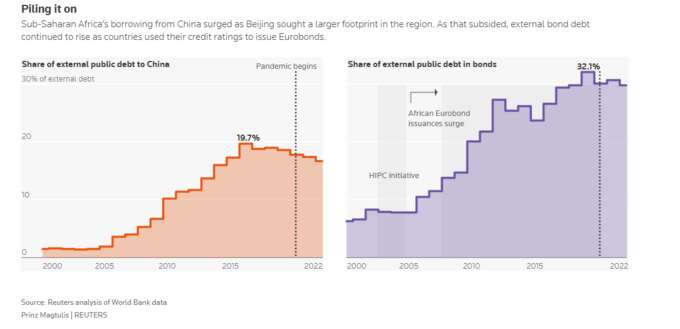

Many countries also leaned more heavily on bond markets as another major source of funding, China, began to pull back. China pushed into sub-Saharan Africa at the start of the new century, and by 2016, it accounted for nearly 20% of the region’s external public debt, according to a Reuters analysis of World Bank data. It has since reduced such lending, while the region’s public bond debt shot up from about 6% of the total in 2000 to more than 32% in 2019.

Some countries used credit ratings and the cash they unlocked to positive effect without blowing out their budgets. With $400 million raised in a 2013 Eurobond issue, tiny Rwanda finished construction of a convention center that has hosted scores of events since it opened in the capital in 2016; bolstered the fast-growing national airline RwandAir; and completed a hydropower project that as of 2020 accounted for about 13% of the nation’s power capacity.

In 2021, Rwanda raised an additional $620 million to pay off the higher-cost $400 million borrowed in 2013 and to fund other projects.

Elsewhere, warning signs flickered.

A drop in oil and other commodities prices in late 2014 dragged down the value of many African currencies, making repayment of dollar-denominated bonds even more expensive. Ghana’s economic growth collapsed to about 2% in 2015. That year, the Ghanaian government, facing a cash squeeze, got a $918 million loan from the IMF. In 2016, interest payments on the government’s debt consumed about 36% of revenue. Nigeria tipped into recession.

As economies teetered, officials often went into spin mode. Foreign investors scouting the region and domestic critics have complained in recent years that officials in Ghana and Nigeria were prone to overstating the health of their economies and sharing data that turned out to be unreliable.

In Nigeria, the Central Bank governor, Godwin Emefiele, continually insisted the country’s currency, the naira, was stable. He labeled those who questioned its value as “unpatriotic.”

“Investors could see right through it,” said Rick Harrell, an emerging markets credit-focused portfolio manager at New York-based Aperture Investors, who attended numerous meetings with other investors from 2017 to 2019.

After Emefiele was suspended from office last year, the Central Bank revealed that under his watch, billions of U.S. dollars of the bank’s foreign exchange reserves were tied up in complex financial contracts. Based on the bank’s official conversion rate at the time, the amount — reported in naira — came to about $32 billion, equivalent to nearly all the nation’s dollar reserves. When the newly elected administration eased controls on the naira last year, the currency tumbled to record lows.

Emefiele is now facing trial on charges of criminal fraud and corruption, including allegations that he gave preferential access to large amounts of foreign currency in exchange for millions of dollars in personal payments from businessmen. He has denied the charges. He did not respond to a request for comment sent through his lawyer.

In Ghana, too, officials could be “terrible” communicators, Harrell said. In meetings he attended between 2017 and 2019, he said, they often contradicted what they had earlier said about the government deficit or financing needs for the energy sector. “It was always a different number every time,” said Boston-based Harrell, whose firm manages $4 billion in assets. Ghanaian media and prominent opposition politician Isaac Adongo have accused the central bank and the government of disseminating misleading data.

The finance ministries in Ghana and Nigeria did not respond to requests for comment about their nations’ record of providing transparent and reliable financial data.

Many of both countries’ grand plans for the money they raised fizzled.

In the prospectus for its debut Eurobond in 2011, Nigeria outlined ambitious goals that included boosting power capacity from about 5,200 megawatts to 40,000 megawatts by 2020. More than a decade on, Nigeria has increased capacity to 12,500 megawatts. Power outages are common, and many people and businesses rely on diesel generators.

In Ghana, a 2018 report produced jointly by the International Growth Centre, a London-based think tank, and Ghana’s civil service found that, due mainly to poor financial planning, a third of local government infrastructure projects — ranging from schools and roads to local infirmaries — were left unfinished after spending some $25 million a year on them.

Outright corruption sank Mozambique’s foray into global finance in what has become known as the tuna bond scandal.

In 2013, Mozambique’s state-owned fishing company began issuing hundreds of millions of dollars in bonds with the stated aim of bulking up the nation’s tuna catch.

International lenders and the rating agencies were caught off-guard when it was revealed, after a restructuring of the bonds in 2016, that the government had also guaranteed an additional $1.4 billion in previously undisclosed loans for the project. That disclosure led to Mozambique’s default. At the time, two dozen fishing vessels bought during the tuna bond scandal were sitting idle in the harbor of Mozambique’s capital.

An IMF-requested audit was unable to determine how at least $500 million raised in the flurry of bonds and loans had been spent. The Mozambique government has maintained that it was the victim of a conspiracy among banks, shipbuilders and corrupt officials. The main bank involved paid hundreds of millions of dollars to Mozambique and U.S. and U.K. authorities, using a mix of cash and debt forgiveness, to settle bribery and fraud allegations.

‘DANTE’S INFERNO’

Already carrying a large amount of debt, Ghana in 2019 broke ground on plans for the nearly $1 billion Pwalugu Multi-Purpose Dam Project. A dream of Ghanaian leaders since the 1960s, the project would tame the sometimes lethal annual floods on the White Volta river, generate power, create fisheries and provide irrigation to farmers — enough to reduce national imports of rice and maize by 16% and 32%, respectively.

In February 2020, Ghana raised $3 billion for the dam and many other projects with bonds issued at rates between 6.375% and 8.875%. It earmarked $75 million of the proceeds for the first year of Pwalugu’s costs, according to a February 2020 government report.

Then COVID hit. The Pwalugu project proceeded haltingly. Staff conducted impact assessments and set up a temporary workers camp. In April 2020, as the pandemic hammered finances, leading to rapid-fire downgrades to ratings and outlooks across sub-Saharan Africa, Ghana’s then-finance minister, Ken Ofori-Atta, wrote in a first-person essay: “Are the rating agencies beginning to tip our world into the first circle of Dante’s Inferno?”

Ghana’s economy stalled, and debt payments soon overwhelmed government spending. Eurobond borrowing costs skyrocketed. To free up money for debt service, the government started cutting other spending. The Ministry of Energy, which helped oversee the dam project, complained of an “inadequate” federal budget allocation for 2021.

In February 2022, Moody’s cut Ghana’s credit rating, squeezing the country’s access to financial markets. Later that year, just before Ghana defaulted on its debt, farmers near the proposed dam complained about what they called an abandoned project; the Pwalugu site had been turned into a bean farm, according to a Ghanaian media report.

The high cost of borrowing effectively killed the project, said Pon Souvannaseng, a professor at Bentley University in Massachusetts who co-wrote a 2022 paper on dam financing in Ghana.

If Africa wants to really become the continent it’s projected to be, you can’t avoid the capital markets. That’s the way of the world.

Daniel Cash, associate professor of law at Aston University in Birmingham, England

The episode shows how developing countries are stuck between two undesirable options for development financing, Souvannaseng said. With long-term, low-cost multilateral lenders like the World Bank, she said, the “the bureaucratic process … to get money — it’s long, it’s tedious, a lot of them find it very humiliating.” But the “high risk, high reward” international bond market, while a quick source of money, “is first and foremost concerned with yield, not with developmental aims,” she said.

Ayhan Kose, deputy chief economist at the World Bank Group, said access to international capital isn’t to blame for Africa’s current debt levels. It’s what happens, he said, when any developing country borrows at an interest rate much higher than its rate of economic growth. “The problem,” he said, “was in their decision to borrow and spend without caution.”

Of the 30 sub-Saharan African nations that now have credit ratings, all but two are rated below investment grade. Since the ratings program began, seven sub-Saharan nations have defaulted on their Eurobonds, some on multiple issuances. Ghana is wrapping up a debt restructuring with its creditors, while Ethiopia is in the midst of its own restructuring talks. Kenya averted default on a looming Eurobond maturity early this year by borrowing more, at just over 10%. But fiscal pressure persists; Moody’s downgraded Kenya deeper into junk territory after the recent riots forced the government to scrap the tax increases that would have made the nation’s debt more sustainable.

The African Union has announced plans to help launch an Africa-based credit rating agency to counter what it says is negative bias among the Big Three. This new agency wouldn’t replace the Big Three for Africa, but its ratings would be "key to addressing the occasional prejudicial credit ratings,” the AU said in a July 2024 press release.

Misheck Mutize, the AU’s lead expert for country support on rating agencies, said in a statement emailed to Reuters that the initial ratings push “was noble to open space for African governments.” But it became clear, he said, that the agencies were “not willing to invest more in understanding African economies.” And today, Mutize said, “the negative narrative has overshadowed all the potential in these countries, and the self fulfilling prophesy keeps the ratings low.”

Most big investors are bound by regulations in their home countries or their own rules on which ratings they can use to manage retirement funds and individuals’ savings. That means, in practical terms, that they would not be able to rely on the African agency’s scores. So for now, Big Three ratings are the only way African countries can reach investors to fund large development projects.

Many African countries count their post-colonial independence in decades and are still building the financial and economic infrastructure that can engage with global capital markets, said Daniel Cash, an associate professor of law at Aston University in Birmingham, England, where he heads a credit rating research program and has written extensively about ratings agencies.

“If Africa wants to really become the continent it’s projected to be, you can’t avoid the capital markets,” Cash said. “That’s the way of the world,” he added.

The Technology Roundup newsletter brings the latest news and trends straight to your inbox. Sign up here.

Reporting by Libby George, Tom Bergin and Tom Wilson in London and Lawrence Delevingne in Boston. Additional reporting by Karin Strohecker in London, Maxwell Akalaare Adombila in Accra, MacDonald Dzirutwe in Lagos, Duncan Miriri in Nairobi, Bate Felix in Dakar, Chris Mfula in Lusaka, Nyasha Nyaungwa in Windhoek, and Loucoumane Coulibaly in Abidjan. Photo editing by Simon Newman. Graphics by Prinz Magtulis and Sam Hart. Design by Jillian Kumagai. Edited by Tom Lasseter and John Blanton.

Source: Reuters