Bank of England warns global wave of elections could impact UK financial system

Central bank raises concerns over newly elected governments as more than 80 countries go to polls this year

Uncertainty caused by a global wave of elections, starting this weekend in France, risks destabilising the UK’s financial system, the Bank of England has warned.

Officials are concerned about the kind of policies that newly elected governments may enforce in large economies, including the US, where Donald Trump is vying for another term as president in the run-up to the election in November.

The French president Emmanuel Macron’s shock announcement of a parliamentary election, with a first round of voting on 30 June and Marine Le Pen’s far-right National Rally party forecast to make significant gains, had shown how political uncertainty could impact economic growth forecasts and cause volatility in financial markets, affecting government debt prices, the Bank’s financial policy committee (FPC) said.

But it is the sheer number of elections taking place this year that was cause for concern, with more than 80 countries – more than half the world’s population –heading to the polls this year. That includes the UK, where citizens will vote in a general election on 4 July.

“Policy uncertainty associated with upcoming elections globally has increased,” the Bank’s financial stability report said. Questions over a country’s political direction could amplify geopolitical risks, increase government borrowing costs, and lead to further global fragmentation, in a way that was “relevant to UK financial stability”, it said.

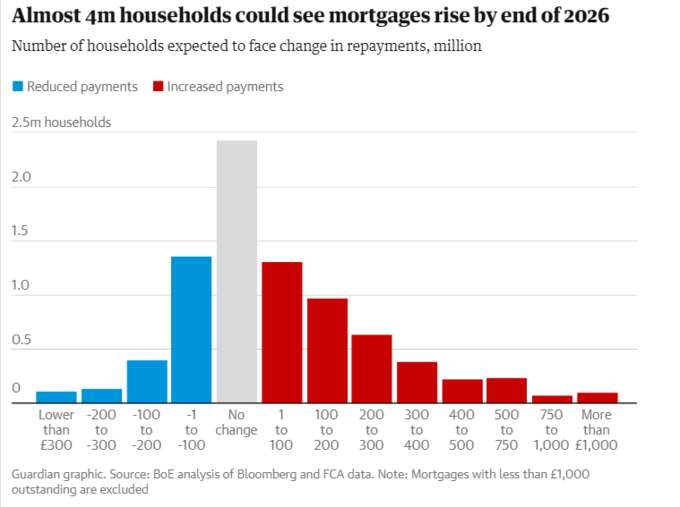

The FPC said it was still monitoring the impact high interest rates were having on households and businesses in the UK, with the Bank’s monetary policy committee having held rates at 5.25% this month for the seventh consecutive time.

That includes the 400,000 households whose monthly mortgage payments are expected to soar by 50% as they roll off fixed rates between now and the end of 2026.

In total, about 3 million – or 35% – of mortgageholders are still on fixed rates of below 3% and are due to see their payments jump over the next two years.

However, if headline interest rates drop from August onwards, as markets predict, another 2 million mortgageholders – including those on variable rates or coming off mortgages set at a higher level – could benefit, offsetting refinancing pressure for some households.

There are also concerns about the financial system’s exposures to the $8tn private-equity industry, which boomed during a period of low interests rates and has grown to play a significant role in financing UK businesses.

“Although the sector has been resilient so far, it is facing challenges in the higher rate environment,” the FPC said, noting this was becoming apparent as firms were forced to refinance their debt at much higher prices.

The FPC said it had also found “gaps” in the way UK banks were managing their exposure to the private-equity industry. The Bank of England and Financial Conduct Authority said they were working together to address a lack of transparency in overall borrowing levels, as well as the valuation of private-equity firms and their investments.

Policymakers said they would continue to test the resilience of the UK’s banking sector, revealing they would be testing the industry against the possibility of two separate and “severe” economic shocks.

The first – a “supply-shock scenario” echoing the ripple effects of Russia’s invasion of Ukraine – would cause inflation and interest rates to soar to 12% and 9%, respectively, as geopolitical tensions disrupt supply chains and cause the price of global commodities to soar.

The second “demand-shock scenario” – which has similarities to the impact of Covid-era lockdowns – assumes demand for global goods and services in decline, sending inflation and interest rates below 0.5% for a prolonged period of time.

In both cases, unemployment is projected to peak at 8.5% and the property industry would take a big hit, with commercial real estate prices declining by nearly 50%.

This year’s so-called desk-based stress tests are the second to be conducted without input from individual banks since they were launched a decade ago in response to the 2008 financial crisis. The Bank of England will not release bank-by-bank results but will issue an aggregate report by the end of the year.

Deputy Editor

Read more similar news:

Comments:

comments powered by Disqus